If you are within a few years of retirement, you may be wondering what a real financial plan actually looks like.

Not a generic calculator. Not a 40-page packet of charts that gets placed in a drawer. A practical, retirement-focused plan that helps answer the questions keeping you up at night:

This article walks through a sample financial plan for Steve and Amanda Doe, a fictional couple approaching retirement. Their example financial plan is designed to show how a modern retirement planning engagement can move from uncertainty to a clear set of decisions, tradeoffs, and next steps.

Steve and Amanda are not real clients. Their details are simplified for education, but their concerns are very real. They want to retire in the same calendar year, around Steve age 65 and Amanda age 61. They want room for travel in early retirement. They also want to understand the maximum spending tolerance of their financial assets — not because they plan to spend every dollar, but because they want boundaries, confidence, and a clear sense of what is possible.

At Peak Financial Planning, we are a fee-only fiduciary financial planning firm focused on retirement income planning for pre-retirees and retirees. Our process is built around a simple philosophy: the plan should lead the investments, not the other way around.

Because this page is meant to function as a true sample financial plan, we will preserve the full client journey rather than only showing a few charts. You will see how an example financial plan moves from goals and documents to retirement income, taxes, investments, implementation, and ongoing monitoring.

Disclaimer

This sample financial plan is for educational purposes only. Steve and Amanda Doe are fictional, and the examples below are hypothetical, simplified, and anonymized. Nothing in this article should be interpreted as individualized tax, legal, investment, or financial advice. Retirement planning recommendations depend on your full financial picture, goals, tax situation, risk tolerance, investment holdings, estate plan, and other personal facts.

Any software screenshots or visual examples referenced below are illustrative, redacted, or anonymized. They are intended to show the type of planning work a client might see, not to guarantee a specific result.

Table of Contents

The Financial Planning Process

The Doe Family Financial Audit

Implementation and Ongoing Planning

Choosing a Financial Planner

Steve and Amanda started where many families start: they had accumulated a meaningful amount of retirement savings, but they did not know how to convert those savings into a confident retirement plan.

They had a 401(k), IRAs, taxable investments, cash reserves, home equity, and future Social Security benefits. They had done a good job saving. But saving for retirement and retiring from those savings are two very different problems.

Their main questions were:

As they searched for a planner, they noticed that firms described financial planning very differently. Some focused mostly on investment management. Some offered one-time advice. Some used planning software but did not specialize in retirement income. Some were insurance-driven. Some charged commissions. Some charged asset-based fees. Some charged flat planning fees.

Steve and Amanda wanted a Certified Financial Planner / CFP® professional who would act as a fiduciary and help them evaluate retirement decisions before talking about investment products or portfolio management.

That mattered because their biggest retirement questions were not simply, “Which funds should we own?”

Their bigger questions were:

That is why they looked for a fee-only fiduciary financial planner with a retirement income planning process, not just an investment pitch.

The Initial Consultation

The initial consultation was not a full planning meeting. It was a fit conversation.

The goal was to understand Steve and Amanda’s situation, clarify what they were trying to solve, and determine whether Peak’s planning process was appropriate for them.

During the conversation, Steve and Amanda shared that:

A good retirement planning consultation should not feel like a product demo. It should feel like a thoughtful diagnosis.

For Steve and Amanda, the key issue was not that they lacked discipline. It was that they had too many unanswered planning questions sitting on top of each other:

This is why a retirement financial plan example is more useful when it shows the full planning sequence. A plan is not one calculation. It is a coordinated set of decisions.

The Financial Planning Process

Peak’s planning engagement is typically a four-month, flat-fee financial planning process. The current planning fee is $8,000. After the planning engagement, clients may choose to implement on their own or transition to ongoing investment management with Peak. For clients who transition to ongoing management, the planning fee may be waived, depending on the arrangement.

The point of the process is not to pressure someone into ongoing management. The point is to help them understand their retirement options clearly enough to make good decisions.

For Steve and Amanda, the process was organized around four meetings:

Before those meetings, Steve and Amanda completed data gathering. To make the data collection process simple, Peak invited Steve and Amanda to a project management tool called Arrows. Arrows include a list of tasks paired with easy to follow walkthrough videos that guide them through the entire data collection process in a matter of minutes. The data collection process included information such as:

Data gathering is not busywork. It is what allows a planner to move from vague advice to a real financial plan example that connects the dots.

Without accurate data, retirement planning can become a pile of assumptions. With accurate data, the conversation becomes much more useful: “Here is what your current path supports, here is what an earlier retirement would require, and here is how we would monitor the plan over time.”

The Doe Family Financial Audit

Before the first strategy meeting, Peak organized Steve and Amanda’s financial picture into a planning baseline.

Their fictional profile looked roughly like this:

That last question is important.

Steve and Amanda were not asking because they wanted to spend recklessly. They wanted to understand the boundaries of the plan.

Many retirees underspend because they never receive a clear answer to, “What can we afford?” Others overspend because they rely on rules of thumb that do not account for taxes, market volatility, life expectancy, Social Security timing, healthcare costs, or future spending changes.

A strong personal financial plan sample should help clients understand both sides:

For Steve and Amanda, the audit also identified several planning issues to explore:

Meeting 1: The Plan Proposal

The first major planning meeting answered Steve and Amanda’s central question:

Can we retire?

More specifically:

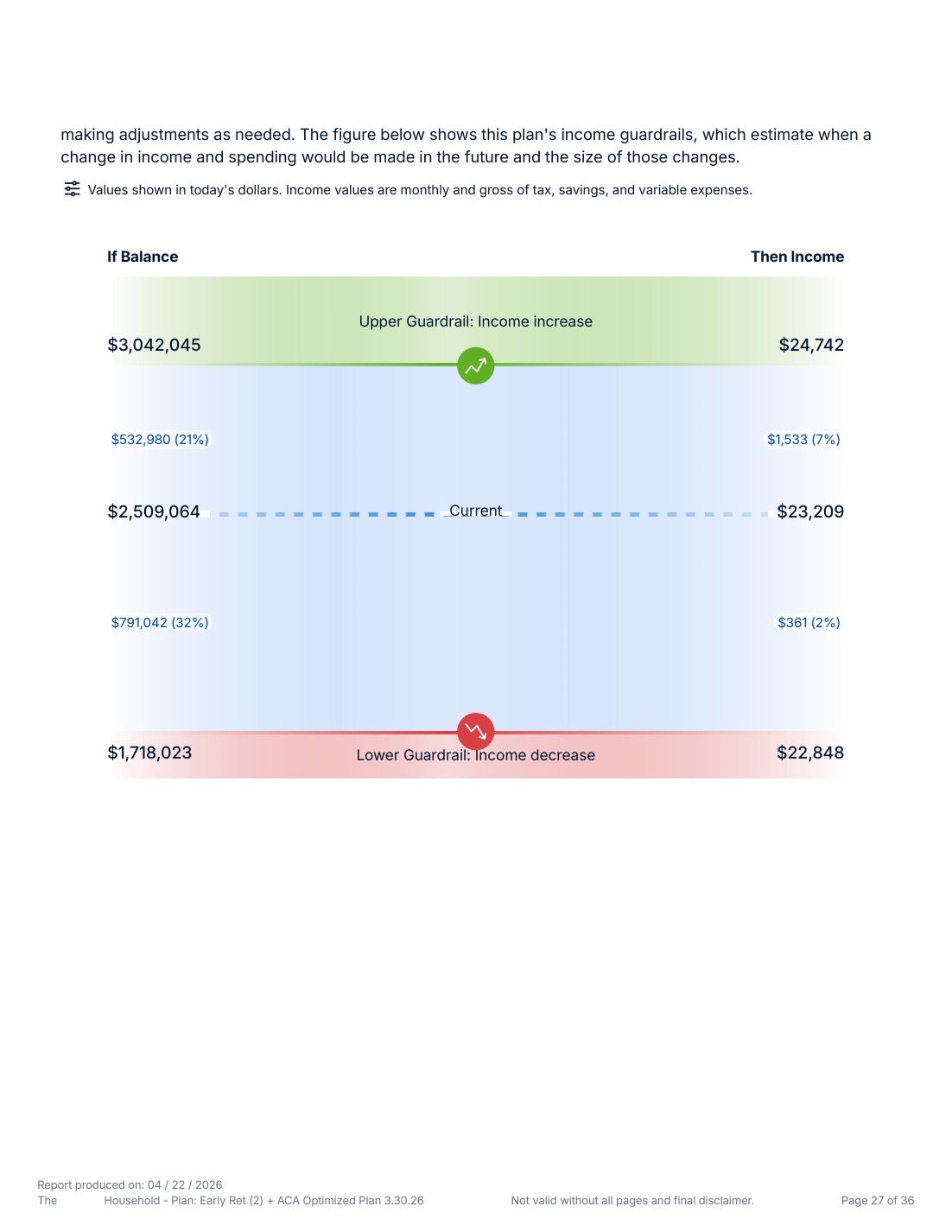

At Peak, this part of the process often uses IncomeLab and a Modern Guardrails framework.

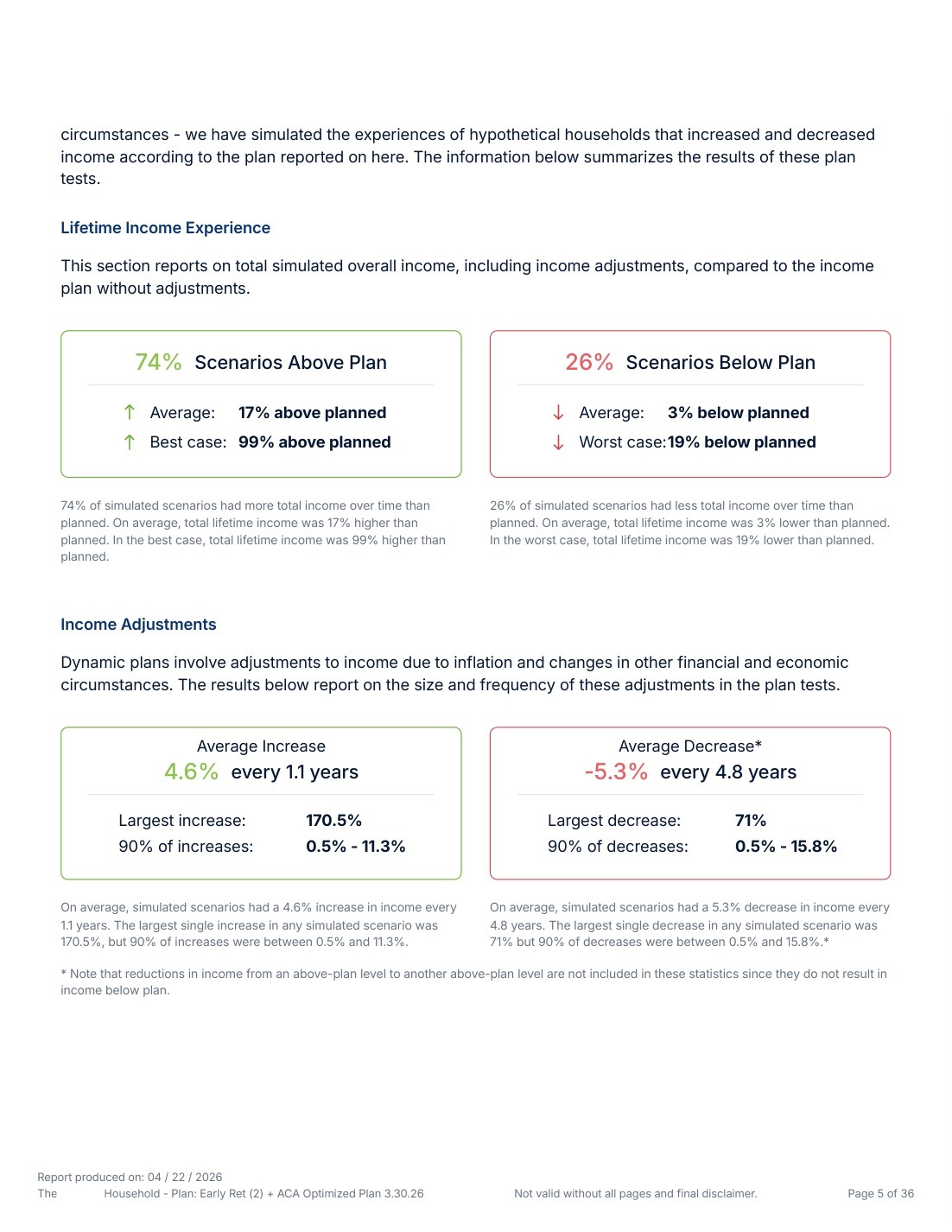

Traditional retirement projections often focus heavily on a probability score: for example, “You have an 87% probability of success.” That can be useful, but it can also create false precision. Retirement is not static. Spending, markets, inflation, taxes, health, and goals change.

Guardrails are different. They are designed to help monitor the plan dynamically.

Instead of pretending that one projection will remain true for 30 years, guardrails help answer:

For Steve and Amanda, the Plan Proposal meeting explored several scenarios.

Scenario 1: Retire as planned

Steve retires around 65. Amanda retires around 61. They maintain their desired lifestyle and include a dedicated travel budget during the first stage of retirement.

This scenario tested whether their base plan was reasonable.

Scenario 2: Retire earlier

Steve and Amanda also wanted to know whether they could retire earlier than planned. The question was not simply whether the software could make the numbers work. The question was whether the earlier retirement date was responsible given their spending goals, tax picture, healthcare costs, and market risk.

An earlier retirement date can affect:

Scenario 3: Higher early retirement travel

Steve and Amanda wanted to travel more while they were healthy and newly retired. That is common. Many retirees do not spend in a perfectly flat line. They may spend more in their go-go years, slow down later, and then potentially face higher healthcare costs late in life.

A useful sample financial plan should reflect how people actually live.

For the Does, the planning conversation separated core lifestyle spending from additional travel spending so they could understand what was flexible and what was essential.

Spending capacity and guardrail validation

A key part of the Plan Proposal meeting was estimating Steve and Amanda’s spending capacity.

Spending capacity is not a command to spend. It is a planning boundary. It helps answer, “Based on the current facts and assumptions, what level of spending appears reasonable?”

Peak may also evaluate whether a proposed plan passes certain validation checks. For example, a plan may be more compelling when:

These are not guarantees. They are planning tools. The goal is to help clients avoid both dangerous overconfidence and unnecessary fear.

For Steve and Amanda, the Plan Proposal meeting ended with a clearer understanding of:

This is where a good financial plan example starts to become practical. The question shifts from “Are we okay?” to “Here are the levers we can pull, and here is how each lever changes the plan.”

Meeting 2: Cash Flow & Taxes

Once Steve and Amanda had a clearer retirement date and spending target, the next question was:

How do we execute this?

This is where many retirement plans become real.

A retirement projection may say a couple can spend a certain amount, but it still needs to answer:

For Steve and Amanda, the Cash Flow & Taxes meeting focused on building a retirement paycheck and a tax-aware withdrawal strategy.

Retirement paycheck

During their working years, Steve and Amanda’s paycheck arrived automatically. Retirement requires intentionally replacing that paycheck.

Their retirement paycheck strategy needed to consider:

A retirement paycheck is not just a transfer from an investment account. It is the operating system for retirement cash flow.

Social Security timing

Steve and Amanda also needed to evaluate Social Security timing.

Claiming early can provide income sooner, but it may reduce lifetime benefits. Delaying can increase monthly benefits, but it requires other assets to fund the gap. The right answer depends on health, longevity expectations, spouse benefits, survivor benefits, taxes, cash flow needs, and the strength of the overall plan.

For many married couples, Social Security is not two separate decisions. It is a household decision.

In Steve and Amanda’s case, the plan evaluated how different claiming ages affected:

Withdrawal sequencing

Withdrawal sequencing is the order in which accounts are used to fund retirement spending.

Steve and Amanda had several account types:

Each account type has different tax treatment. Pulling from the wrong account at the wrong time can create unnecessary taxes or reduce future flexibility. But tax minimization should not become the only goal.

The better question is: which withdrawal strategy best supports the retirement lifestyle while keeping taxes reasonably efficient?

Roth conversions

Roth conversions were also evaluated.

A Roth conversion means moving money from a pre-tax retirement account to a Roth account and paying tax on the converted amount now. The potential benefit is that future growth and qualified withdrawals may be tax-free.

For pre-retirees and retirees, Roth conversions may be attractive during lower-income years after retirement and before required minimum distributions begin. But they are not automatically good. They can increase current taxes, affect ACA subsidies, increase Medicare IRMAA premiums in future years, and reduce liquidity if taxes are paid from outside assets.

For Steve and Amanda, Roth conversions were considered as one tool inside the broader plan — not as the plan itself.

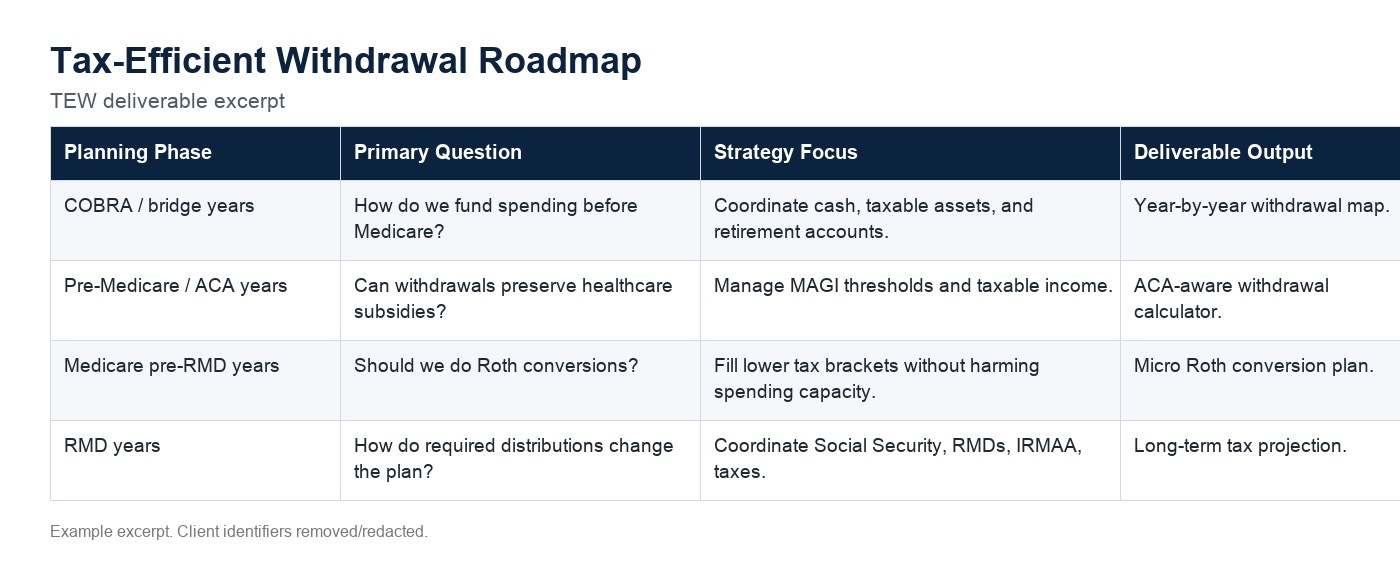

Retirement tax phases

Steve and Amanda’s retirement tax picture changed across phases:

A tax-efficient withdrawal roadmap can help coordinate these years.

The goal was not to make Steve and Amanda tax experts. The goal was to give them a clear sequence:

This is an important distinction. Retirement tax planning should serve the life plan. It should not become a game of minimizing taxes at the expense of flexibility, spending confidence, or peace of mind.

Meeting 3: Investments 1

After the retirement income plan and tax roadmap were developed, the next question was:

Is the portfolio built for this plan?

This is where Peak’s philosophy matters: plans lead investments.

Many people start with investment performance and then try to back into a retirement plan. Steve and Amanda needed the reverse. They needed to know what kind of portfolio could support their income plan, risk tolerance, and guardrail framework.

The Investments 1 meeting reviewed their current portfolio through several lenses.

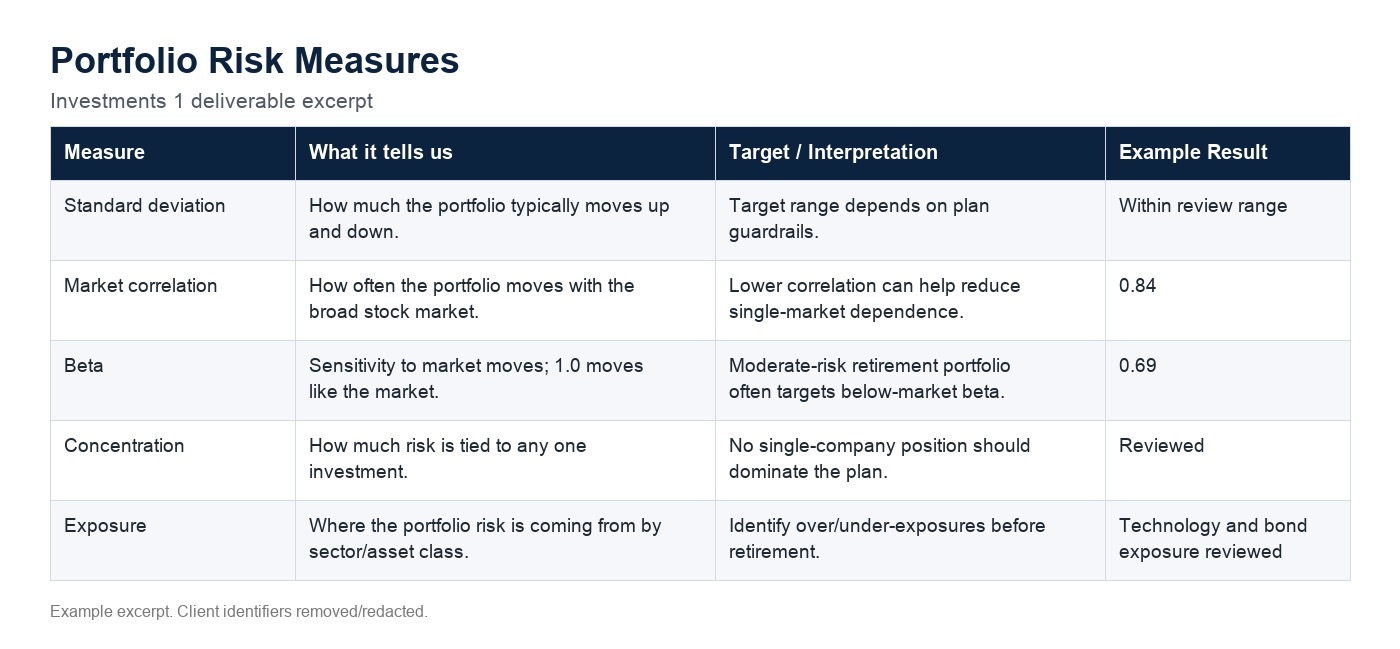

Portfolio risk audit

Peak may use tools such as Nitrogen to evaluate portfolio risk. The goal is not to reduce a portfolio to one score, but to understand how the portfolio behaves.

For Steve and Amanda, the review looked at areas such as:

Why risk matters differently in retirement

During accumulation, a market decline is uncomfortable. During retirement, a market decline can be more complicated because withdrawals may be occurring at the same time.

This is often called sequence-of-returns risk. If a retiree is taking withdrawals while the portfolio is down, losses may be harder to recover from, especially early in retirement.

That does not mean retirees should avoid market risk entirely. Growth still matters, especially for a retirement that may last 25 to 35 years. But the level of risk should be connected to the plan.

For Steve and Amanda, the investment conversation focused on questions like:

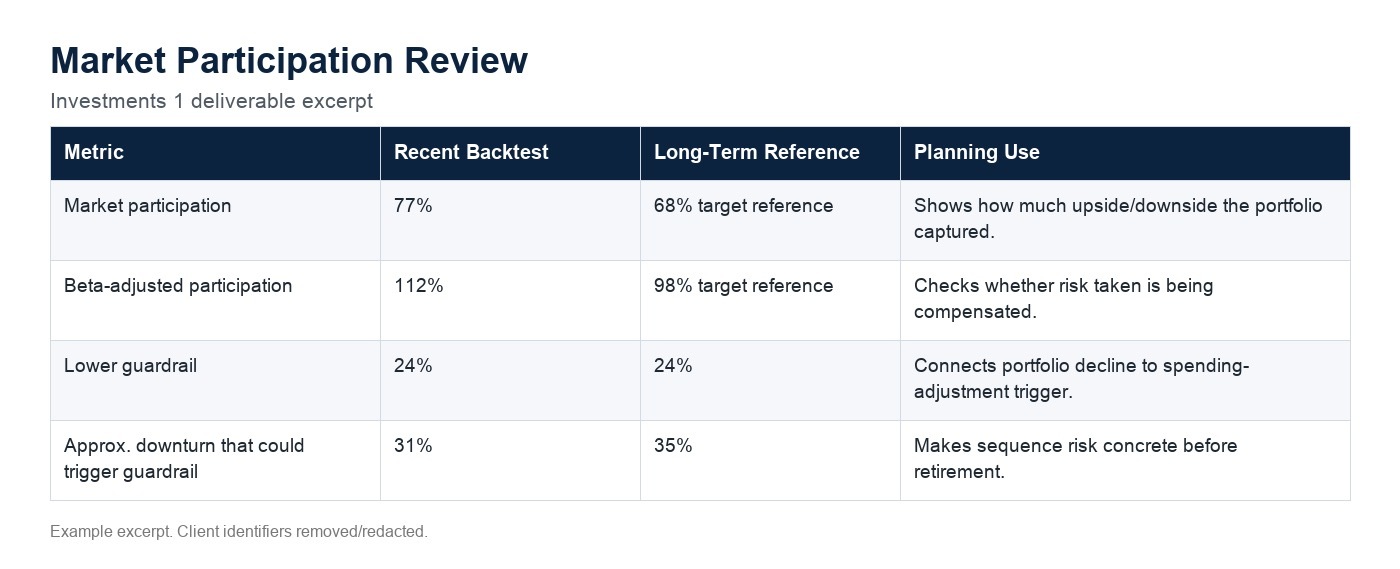

Market participation

The plan also considered market participation — how much of the portfolio’s movement may be expected to participate in broader market gains and losses.

Steve and Amanda did not need a portfolio that looked impressive on paper. They needed a portfolio that supported their actual retirement income plan.

That meant evaluating whether their investments matched:

The output of this meeting was not simply “buy this” or “sell that.” It was a clear understanding of whether their current portfolio was aligned with the plan, and what changes might be considered if they wanted a more coordinated strategy.

Meeting 4: Investments 2

The fourth meeting answered the next practical question:

What does implementation and ongoing management look like?

By this point, Steve and Amanda had reviewed:

Now they need to decide how to implement it.

Some clients want a plan and prefer to manage implementation on their own. Others want ongoing help because they do not want to manage portfolio changes, withdrawal coordination, tax-aware rebalancing, account consolidation, or annual planning updates by themselves.

Both choices can be reasonable. The key is that the client understands what they are choosing.

If Steve and Amanda self-manage

If Steve and Amanda chose to implement on their own, their financial plan would give them a roadmap. They would still need to coordinate with their tax professional, update the plan over time, place trades if needed, manage cash flow, evaluate Roth conversions annually, and revisit Social Security timing as they approached claiming decisions.

Self-management may work well for retirees who are organized, comfortable with investments, and willing to maintain the plan.

If Steve and Amanda hire Peak for ongoing management

If Steve and Amanda chose ongoing investment management with Peak, the relationship would shift from a planning project to an ongoing advisory relationship.

Ongoing management could include items such as:

This should be transparent and non-pushy. Ongoing management is not necessary for every person, and no advisory relationship can guarantee investment outcomes or eliminate risk.

For Steve and Amanda, the key question was not, “Can someone beat the market for us?”

The better question was, “Do we want a professional team helping us keep this retirement plan organized, updated, and implemented over time?”

Implementation and Ongoing Planning

A financial plan is only useful if it changes decisions.

For Steve and Amanda, implementation included a prioritized action list. Depending on the final recommendations, this could include:

The plan was not a one-time prediction. It became a decision-making framework.

That matters because retirement is full of moving parts. Markets change. Tax laws change. Health changes. Spending changes. Family circumstances change. A retiree may start with one travel goal and later decide to help children, move homes, give more to charity, or spend differently than expected.

A good financial planning process should not pretend the future is fixed. It should give clients a way to adapt.

For Steve and Amanda, the final plan gave them three important forms of clarity:

That is the real value of a comprehensive sample financial plan. It is not about producing a binder. It is about helping real people make better retirement decisions with less guesswork.

Frequently Asked Questions

What is a sample financial plan?

A sample financial plan is an educational example that shows what a financial planning engagement may include. It often uses fictional clients, simplified assumptions, and sample deliverables to explain the planning process.

A good sample should show more than charts. It should explain the questions being answered, the assumptions being used, and how recommendations connect to the client's goals.

Is Steve and Amanda Doe's plan a real client plan?

No. Steve and Amanda Doe are fictional characters. Their plan is an example only and should not be treated as advice for any specific person.

What should an example financial plan include?

An example financial plan may include retirement projections, cash flow planning, tax planning, Social Security analysis, withdrawal sequencing, investment review, insurance review, estate planning considerations, and implementation steps.

For retirees and pre-retirees, the most important parts often include retirement date analysis, spending capacity, retirement paycheck design, tax-efficient withdrawals, and portfolio risk alignment.

What is the difference between a financial plan and an investment proposal?

An investment proposal usually focuses on how money should be invested. A financial plan is broader. It connects investments to retirement income, taxes, spending, Social Security, estate planning, insurance, and personal goals.

At Peak, the plan leads the investments. The portfolio should be designed around what the retirement plan needs, not the other way around.

What is a retirement financial plan example?

A retirement financial plan example shows how a household might evaluate retirement readiness, spending capacity, income sources, taxes, withdrawals, Social Security, Medicare, and investment risk.

For Steve and Amanda, the retirement plan focuses on whether they can retire in the same calendar year, how much they can spend, how to create a retirement paycheck, and how to align their portfolio with the plan.

What is a personal financial plan sample?

A personal financial plan sample is a fictional or anonymized example of a financial plan for an individual or household. It helps prospective clients understand the structure, depth, and types of recommendations they might receive.

The important word is “sample.” Your actual plan should be based on your own facts, goals, accounts, taxes, and risk tolerance.

How does the financial planning process work?

The financial planning process typically starts with discovery and data gathering. The planner then analyzes your current situation, identifies major planning decisions, models different scenarios, and develops recommendations.

Peak's retirement planning process is organized around four meetings:

How much does Peak's planning engagement cost?

Peak's planning engagement is typically an $8,000 flat-fee, four-month financial planning engagement. Some clients choose to implement the recommendations themselves. Others choose to transition to ongoing investment management. For clients who transition, the planning fee may be waived.

The right option depends on the complexity of your situation and how much support you want after the plan is built.

Do I have to hire Peak to manage my investments?

No. The planning engagement can stand on its own. Some clients complete the plan and implement independently.

If you want ongoing support, Peak can explain what investment management would include, what it costs, and how it would connect to your retirement income plan. The decision should be clear and non-pressured.

What is a fee-only fiduciary financial planner?

A fee-only fiduciary financial planner is compensated directly by clients and is obligated to put clients' interests first. Fee-only planners do not receive commissions for selling financial products.

This structure can help reduce conflicts of interest, although it does not eliminate the need to evaluate an advisor's expertise, process, communication style, and fit.

Why work with a Certified Financial Planner / CFP® professional?

A Certified Financial Planner / CFP® professional has completed education, examination, experience, and ethics requirements related to financial planning. For retirement planning, it can be valuable to work with someone trained across investments, taxes, insurance, retirement, estate planning, and cash flow.

Credentials are not the only factor, but they can be an important starting point.

What are retirement guardrails?

Retirement guardrails are a dynamic planning framework used to monitor spending over time. Instead of treating retirement as a one-time probability score, guardrails help define when spending may be increased, maintained, or reduced based on portfolio performance and plan conditions.

Guardrails do not guarantee success. They provide a structured way to make adjustments as reality unfolds.

Why not just use a retirement calculator?

Retirement calculators can be useful, but they are usually limited. Many calculators do not fully account for tax strategy, Social Security timing, withdrawal sequencing, Medicare IRMAA, Roth conversions, changing spending phases, or portfolio construction.

A calculator may tell you whether you are broadly on track. A planning process should help you decide what to do next.

How should taxes fit into a retirement plan?

Tax planning should support the retirement lifestyle plan. It may include withdrawal sequencing, Roth conversions, capital gains planning, charitable giving strategies, Social Security taxation, Medicare IRMAA awareness, and required minimum distribution planning.

The goal is not always to minimize taxes in a single year. Often, the goal is to improve after-tax flexibility over the full retirement timeline.

What is a Tax-Efficient Withdrawal roadmap?

A Tax-Efficient Withdrawal roadmap shows which accounts may be used for retirement income during different years. It helps coordinate taxable accounts, traditional IRAs, Roth IRAs, Social Security, pensions, and required minimum distributions.

For retirees, this can be one of the most practical deliverables because it turns the plan into a year-by-year retirement paycheck strategy.

Should everyone do Roth conversions before retirement?

No. Roth conversions can be helpful in some situations, especially during lower-income years before required minimum distributions begin. But they are not automatically the right move.

A Roth conversion decision should consider current and future tax brackets, Medicare IRMAA thresholds, ACA subsidies, estate goals, cash flow needs, and the source of funds used to pay the tax.

How does Social Security fit into a financial plan?

Social Security is a major part of many retirement plans. Claiming decisions can affect lifetime income, survivor benefits, portfolio withdrawals, tax planning, and retirement flexibility.

The right claiming strategy depends on health, life expectancy, marital status, benefit amounts, cash flow needs, and other income sources.

Why does the investment portfolio need to connect to the financial plan?

Because investments are not separate from retirement income. A portfolio that looks reasonable in isolation may not be appropriate for the client's withdrawal needs, tax situation, guardrails, or risk tolerance.

In retirement, the portfolio has to support spending while managing volatility, liquidity, taxes, and long-term growth needs.

What happens if markets decline after retirement?

A market decline early in retirement can put pressure on a plan, especially if withdrawals are beginning at the same time. This is sometimes called sequence-of-returns risk.

A good retirement plan should address this possibility through appropriate portfolio design, cash flow planning, guardrails, flexible spending, and ongoing monitoring.

How often should a financial plan be updated?

A financial plan should be updated whenever major assumptions change. That may include retirement timing, spending, investment returns, tax laws, health events, family needs, or estate goals.

For retirees, annual reviews are often useful because withdrawal decisions, tax planning, and portfolio management are ongoing.

Can a financial plan guarantee that I will not run out of money?

No. No responsible planner can guarantee that. Markets, inflation, longevity, tax law, health care costs, and personal circumstances are uncertain.

The purpose of planning is not to eliminate uncertainty. It is to create a thoughtful decision-making framework, identify risks, build flexibility, and monitor the plan over time.

Next Step

If you are approaching retirement and want to understand what your own financial plan could look like, the next step is to start with a structured retirement planning conversation.

You do not need to have every answer before meeting with a planner. You just need the right questions:

Steve and Amanda Doe's story is fictional, but the planning journey is familiar. Retirement is too important to navigate with guesswork, generic calculators, or investment recommendations disconnected from your actual life.

If you would like to explore Peak Financial Planning's process, you can start here: